The Financial Mechanics: Inflation Erosion & Opportunity Cost

Every tax season, millions of Americans celebrate their refunds like a financial windfall. But a refund is not a government gift — it is merely the return of your own money that you allowed the U.S. government to hold interest-free throughout the year, at significant personal and societal cost.

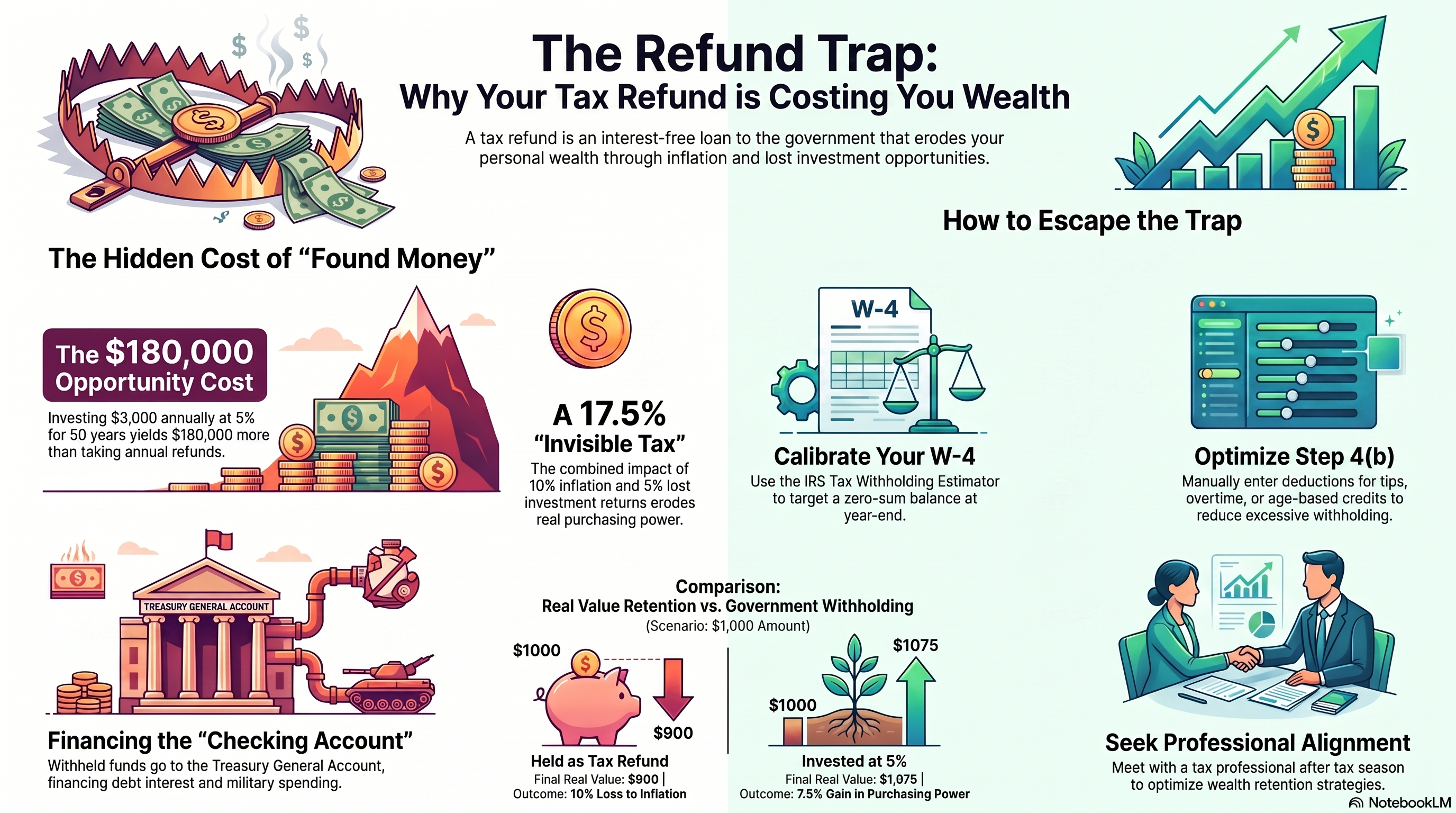

A large refund means you overpaid federal taxes through excessive payroll withholding (see Box 2 of your W-2). That's an interest-free loan to the government — money that could have been invested, saved, or used to pay down debt all year long.

Inflation makes it worse: while the government holds your money, its purchasing power erodes. A $1,000 refund with 10% inflation loses about $100 in real value — while the same $1,000 invested at 5% would have gained about $75. The refund's psychological appeal as "found money" exploits present bias and mental accounting, keeping taxpayers blind to the opportunity cost — and to the slow drain on their family's generational wealth.

Watch: The Refund Trap (Captioned)

If the video does not appear, place the file "The Refund Trap (captioned).html" in the same folder as this page. It requires JavaScript to display.

Let's see what bigger refunds signify in this scenario: A refund of $3,000 per year that could instead be invested at 5% grows to over $330,000 across 50 working years. This hits families especially hard: people with children often receive some of the largest refunds while still paying federal withholding out of every paycheck all year long — meaning both the overwithheld dollars and the credit money sit with the government, interest-free, until refund season.

A Note on Inflation

Inflation is usually officially stated at around 2–4%, and it is currently on the high end of that range. The reality is that inflation normally hovers around 6–8%, and depending on what you spend money on, 10% is very possible. The scenarios above are based on 10% for that possibility, and for simplicity in rounding.

Where Your Withholding Actually Goes

Your withholdings are not held in a separate account for your refund. All federal tax withholdings are deposited into the U.S. Treasury General Account (TGA) at the Federal Reserve — effectively the government's checking account — which pays for military spending, interest on the national debt, federal agencies, foreign aid, and everything else Congress authorizes. Even "dedicated" Social Security and Medicare payroll taxes end up financing general operations in real time, with the trusts receiving Treasury IOUs.

This pool of interest-free capital masks the true size of deficits and reduces pressure on lawmakers to be fiscally accountable. In fiscal year 2025 the U.S. government spent about $970 billion on net interest payments — nearly 20% of federal revenue. Financial thinkers like Ray Dalio have warned that unchecked debt spending and money printing threaten global economic stability (see Ray Dalio warns on unsustainable debt, CNBC). There are also moral dimensions of what pre-collected taxpayer capital underwrites, from a ~$997 billion military budget (roughly 37–40% of all global military spending in 2024) to expanded immigration-enforcement appropriations.

How to Escape the Refund Trap

- Stay under the penalty line. The simple rule: don't owe more than $1,000 in federal tax at year's end, and you avoid the Underpayment of Estimated Tax by Individuals Penalty. Owing a small amount, planned well, is the best-case scenario.

- Use the IRS Tax Withholding Estimator to target near-zero refund and near-zero balance due. Note it may lag behind newer deductions such as tips, overtime, and over-65 deductions.

- File a new Form W-4 with your employer — as often as needed. Marriage, children, or job/salary changes all warrant a revision; even a post-revision paycheck review may prompt another.

- Consider Step 4(b). Rather than leaving it blank (which tends to overwithhold), enter relevant deduction amounts — tips, roughly one-third of expected overtime, at least $6,000 if over 65, and planned Traditional IRA contributions.

It is a good idea to consult an experienced tax professional — one who will spend real time with you — to optimize your W-4 and learn about tools such as IRAs that build wealth and generate tax savings. After tax season is often the best time to book that appointment.

Have questions about your own withholding? I would be happy to set up a time for a free consult on tax information — just reach out through the contact page.